The authors offer a useful reminder of just how widely scholarly estimates of output and intake continue to diverge after (or even because of?) all the painstaking work of the likes of Campbell-Overton, Turner, Allen and the wayward Clark. Even the rival estimates cited for grain yields in 1800 (probably one of the less contentious topics!) vary by 15-30% for individual crops, and the margin of disagreement widens still further for earlier periods or for livestock produce. It’s hardly surprising that the field is bedevilled by differences of interpretation and periodisation, but that’s down to our limited sources more than to those who’ve sought to make sense of them.

As in Clark et al’s classic 1995 paper, the authors point to the discrepancy between the demand increase expected from rising per capita GDP and sluggish growth in consumption of agricultural produce, though this time the conundrum is placed in a far longer timeframe:

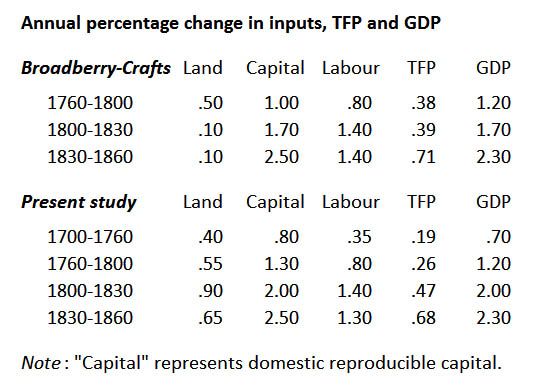

According to Broadberry et al, English GDP per capita trebled between c.1260 and the mid-eighteenth century. What they dub 'modest but positive trend growth' is troubling for their estimates of agricultural output and average calorific intake, since even very low income elasticities are not easily reconciled with zero sustained improvement in calorie supplies over the same period.

"Troubling" is putting it mildly, because with agriculture contributing a third to two-fifths of output in the mid-18th century, a tripling of per capita GDP in the preceding half-millennium would make real starvation the 13th-century norm well before before putative overpopulation and soil exhaustion took their toll. Happily Broadberry’s growth rates work out at "only" 2.3-fold income growth over 1270-1760 (though it’s annoying to have to reconstruct the missing aggregates). And even that’s an overestimate derived from an improbably low late-medieval starting-point entirely obscured by the omission of actual GDP estimates.

The problem is exacerbated by the Broadberry team’s overstatement of early and mid 18th- relative to mid 17th- or mid 19th- century income, the implication of an excessive growth rate in 1650-1700 and improbably low ones in 1760-80 and 1800-30 (population conversely appears understated in relative terms over 1650-1780, though to a lesser extent, though any error is difficult to pinpoint as even this number is absent).

If average income barely doubled over 1270-1760 (as a simple estimation of life’s necessities and the incomes of the non-agricultural population might have suggested had Broadberry & co stuck to quantities rather than churning out speculative growth rates), we’re still left with the apparent food consumption paradox raised by faster growth afterward, a problem masked by their high estimates for 1700 and to a lesser extent 1760 compared to 1830 – which brings us back to the very period of the original and still only partly resolved 1995 "food puzzle".

And unfortunately replacing the Broadberry output index doesn’t help towards raising food output growth at this time, because the 2011 paper offers astonishingly low "current-price" GDP shares for agriculture of 29.7% in 1759 and a frankly incredible (even just by comparison with 1759 and allowing for intervening price movements) 26.7% in 1700. Now it’s true that contemporary estimates leave much to be desired and that recent occupational studies have pointed to a far larger industrial workforce than previously assumed. But even amid generally low cereal prices a real agricultural GDP share significantly under 40% seems unlikely for the first half of the 18th century given the upturn in grain exports and the fact that it remained above a quarter even into the 1820s, combined with the small contribution of industry (only some £25m of English GDP even at mid-century, under £30m for Great Britain).

Kelly & Ó Gráda do identify two possible solutions to the paradox, one explored more fully in the 1995 study, the other potentially only deepening the problem. To take the latter first, they suggest that livestock output was higher in the late 18th century than widely thought. And they’re right: both milk and meat appear underestimated in the Broadberry paper, chiefly reflecting low cattle numbers. The problem here is though that while 18th-century numbers may be understated, the same goes still more for yields in earlier centuries. It’s likely on balance that livestock production grew if anything at a slower rate than these estimates indicate.

The other avenue is far more rewarding. If our evidence conflicts with assumed elasticity of demand for foodstuffs, then either the evidence is wrong or our elasticity is inappropriate. And sure enough, Clark &c pinpointed the solution two decades ago: “What people eat and drink differs from the food products supplied by agriculture and net imports.” And what we spend in addition to the cost of crude foodstuffs rises with income, urbanisation and specialisation and our associated move from farm to retail: this was indeed the case in the 18th and 19th centuries when the share of processing and distribution rose from roughly a fifth of final consumption to 45%.

The difference between the two elasticities is striking for the period under review: 0.55 for final consumption, 0.25 for crude farm produce, both falling over time as we should expect. Transport, processing and trade together contribute 0.30 of the figure for end goods, alone more than doubling the rate. Coupled with higher medieval income at about half of the 1730 average, this suggests growth of rather over two-fifths in per capita consumption of crude foodstuffs over 1270-1870, consistent with 19th-century agricultural output estimates and a late medieval population of four million or so. This result captures both Clark &c’s "food multiplier" and shifts in the balance of overseas foodstuffs trade.

The situation in the key period 1770-1830 is less clear-cut. It seems likely that large sections of the population were unable to enjoy the nutritional opportunity implied by per capita GDP growth. Wartime disruption & inflation and subsequent protection may well have constrained food supply until the more favourable 1830s. But agricultural output data are particularly lacking around the latter part of the period, and it may be that contemporary food expenditure returns have failed to capture some of the undoubted gain since even the grain-surplus years of the mid-18th century.

An implication of the wide elasticity margin is, however, slower agricultural growth than in Overton's estimates - here about 2.6-fold over 1700-1870, consistent with appreciably higher cattle and pig output c.1700 (partly offset by lower sheep numbers) and lower 19th-century milk yields than those assumed in the Broadberry project. Coupled with the Cambridge occupational history project's findings of a larger industrial workforce around 1710, this in turn raises questions about 17th-century labour productivity growth. The Agricultural Revolution is likely to prove a longer affair than aggregate output growth suggests.