Lately catching up with Andrei Markevich and Mark Harrison on Russian/Soviet national income from 1913 to 1928, I’m impressed at the authors’ readiness to dirty their hands filling in the yawning chasm between our available benchmarks for a society transformed in the interim by war, revolution and chaos. I’m less than entirely convinced though by some of their choices in an exploration necessarily hedged to some extent by assumptions in the absence of comprehensive data.

It’s a huge topic, covering the economy of a nearly tenth of the world over a period of traumatic political & social upheaval and rebuilding, complicated by statistical uncerainties throughout and by the legacy of past manipulation and politicisation. Harrison and Markevich try to get to the truth by stripping the economy down to its nuts & bolts, with output series for key sectors weighted according to Falkus’s estimates and brought into line with Gregory’s 1913 national income figure by means of a further allowance for services.

For the most part the data are derived from existing production series, with interpolations for years for which firm figures are missing. Strictly the approach yields an index of gross output rather than value added, but it’s a tried & tested method that underlies most pre-20th-century estimates and for most countries remains the best we have. The resulting totals persuasively flesh out our hitherto sketchy impressions, broadly supporting the accepted picture: aggregate net national income for the territory of the interwar USSR fell by three-fifths in 1913-19, regaining its pre-war level in 1926/27, but income per head remained below the 1913 peak into the Plan era.

The calculation however involves some questionable assumptions which leave open the possibility that the drop may have been rather less precipitous and subsequent recovery more complete (though by no means complete in per capita terms).

First, in addressing the question of population, the authors rightly seek to correct the official population returns for what has long been known to be an ongoing cumulative overstatement arising principally from failure to deduct internal migrants from the estimated population of their former place of residence, while adding them to that of their new location. Deducting Finland and Poland from the population total for the "censused" part of the Empire, they then deduct a “compromise” 5½% to correct the official data, observing that this corresponds fairly closely to the findings of R I Sifman, though the resulting 152m for mid-1913 in fact falls short of Sifman's implied total by upwards of a million.

The authors’ next step is to arrive at a population for the interwar USSR by excising the areas lost after the Revolution: the later Baltic republics, western Belarus & Ukraine, Bessarabia and smaller areas of Transcaucasia. Here, Markevich & Harrison arrive at 19.7 million for the population of the ceded territories, concluding that the interwar USSR area contained 134.6 million people in 1913. But the figure for the lost provinces is inflated by the erroneous inclusion of Podolia, which instead remained a part of Ukraine throughout the USSR’s existence.

Deducting Poland and the corrected estimate for the lost territories from Sifman’s Empire total (which already omits Finland) and adding Khiva & Bukhara (not covered by the Imperial returns) yields a 1913 population of not 134 million but just under 140 million for the USSR area, very close in fact to Lorimer’s 1945 finding which put the ceded provinces at only 14.9 million in January 1914. The result underlines the unwisdom of applying a blanket correction factor across the Empire: while Szulc finds a 7% overcount in Poland, the interwar USSR included the principal receiving areas for internal migrants, so it requires a smaller adjustment than the Empire as a whole or even its non-Polish part. The error doesn’t affect the constant-area national income figure, but it threatens to distort the implied per capita trend.

One assumption that does affect the national income total relates to agriculture, where the authors accept Gosplan’s later upward revisions of pre-Revolutionary crop output. The modification has been widely questioned, as Markevich & Harrison acknowledge, but they propose its retention for 1913-19 in order to being the earlier data into line with the returns for the 1920s. They may be correct in so doing, but most sources retain the unadjusted returns. The Soviet authorities themselves seem later to have abandoned the correction, though this might be dismissed as an attempt to play down relative Soviet underachievement. Naum Jasny, among Soviet agricultural performance’s fiercest critics, seems to have found the original Imperial data satisfactory. The net impact could be to understate 1920s national income by 5% relative to 1913.

The paper’s assumptions don’t all point in the direction of higher pre-revolutionary per capita output. On the perennial question of product quality, the authors make no downward adjustment to Soviet output, observing that while some doubtless fell below pre-revolutionary standards, other sectors shared to some extent in wider technical advance - which might be read as a polite way of noting that the Russia of 1913 was itself hardly famed for cutting-edge finery.

An error that doesn't affect the constant-area national income trend but instead overstates the "Empire" series is the authors' application of the Falkus/Gregory aggregates for the Empire to their own "Empire excluding Poland and Finland". Falkus and Gregory indeed exclude Finland, as did the contemporary imperial returns - but they include Congress Poland, representing nearly a tenth of the total in the truncated form used by Markevich & Harrison (ie following Kholm gubernia's detachment in 1912). The smaller Empire on which the latter base their income figures may have reached the higher income total, but the estimates cited in the paper suggest something lower than the authors' findings. Happily the error doesn't affect the USSR series, which the authors base on Falkus's own Empire-to-Union conversion, itself a good deal more reliable than Gregory's.

All in all it’s a worthwhile effort, let down by some decidedly rickety & inconsistent population estimates and inattention to geographical coverage which could overstate the 1913 Soviet-area per capita income by as much as 4% relative to the 1920s, in addition to a possible far greater over-statement of pre-Revolutionary crop output and high figures for the old Empire. Markevich & Harrison are to be commended for tackling a too long neglected topic, but it remains one which would benefit from closer investigation.

Thursday 7 October 2010

Friday 24 September 2010

Blame France?

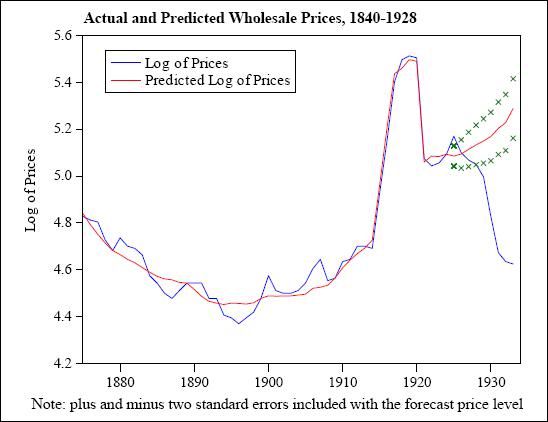

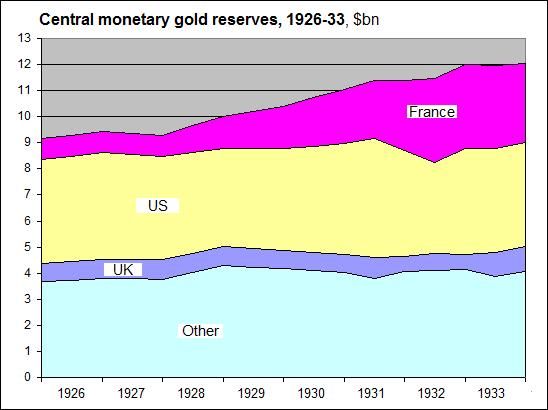

Douglas Irwin isn’t out to spearhead Franco-American rapprochement. “Did France cause the Great Depression?” he asks, and there’s more to the proposition than foreign-policy sour grapes. From 1928 to 1932 the Banque de France gobbled up virtually the world’s entire supply of new central-bank reserve gold – $2.5bn of it – effectively “sterilising” it (i.e. not issuing new money in proportion) when other countries needed it to back up monetary expansion to stave off deflation. The effect was to execerbate a severe global deflationary spiral that lasted until 1933 when the US at last followed Britain in abandoning the gold standard.

Irwin doesn’t at all exonerate US monetary authorities of their share of responsibility for the slump: rather he finds that while the two countries were equally to blame in the first half of the period, France was the culprit after the US reversed its own gold hoarding in 1931. It’s not an entirely novel perspective: Irwin cites contemporary expert warnings of the dangers of French & US conduct even as prices seemed to be stabilising in 1928 and the first half of 1929. What’s new is his finding that world prices would have risen in 1929-33 rather than plunging, had France and the US merely maintained their 1928 ratio of reserve gold to money supply. The associated graph is striking, but not entirely convincing: for one thing, it doesn’t explain falling prices in 1925-28, when French and US gold holdings were reasonably well-behaved and world gold reserves rising broadly in line with economic output; it also doesn’t show what the projected price trend would have been under the same assumptions but with no additional monetary gold from 1928, as was effectively the case. Even with the average world economic growth rate of around 3¾% annually over 1922-29, an absence of extra “active” gold would seem insufficient to account for the scale of the subsequent collapse of prices – and that’s before taking into account the reversal of real output growth in the early 1930s. But it certainly didn’t help.

In fairness to the French, it should be remembered that despite converting a large part of its sterling holdings into gold from 1927, the Banque’s reserves still suffered through Britain’s effective 30% devaluation in 1931. If – as most commentators seem to agree – sterling was indeed overvalued by something like a tenth in 1925, then gold indeed made more sense than at least one of the world’s notional reserve currencies. French gold hoarding of course contributed to sterling’s difficulties, so it’s not much of an excuse. And the franc was itself widely regarded as undervalued from 1928, making the country already a gold sink. Though cushioned to some extent against the first impact of the 1929 global economic downturn, France was to pay dearly for its attachment to gold as she entered the worst phase of the depression just as many countries were starting to climb out of it in 1933: not until 1936 did the country finally free itself of what Keynes had dubbed the gold “fetish”, the last power to do so. By 1938 France’s share of world gold reserves was down from its 1932 peak of 28% to just a tenth.

What are we to make of it all? Well, for one thing proclaiming a new international regime doesn’t make it so without the mechanisms to implement it. Could the gold exchange standard have worked as envisaged at Genoa in 1922? For a time, no doubt, with better alignment of the key currencies and binding undertakings to play the game: supply of the required metal was to prove adequate in the 1930s, as it could have been in the 1920s. But by then it was too late: the inflexibility implicit in the attempt to return to gold and the impossibility of ensuring its optimal distribution had crippled not just the monetary system but the wider economy. Would a more internationally-minded Banque de France have spared the world the nightmare of Depression and war? Possibly not: there was far more amiss in the interwar economy than just monetary policy and gold stocks. France may not have caused the Depression, but it made things a lot worse.

Irwin doesn’t at all exonerate US monetary authorities of their share of responsibility for the slump: rather he finds that while the two countries were equally to blame in the first half of the period, France was the culprit after the US reversed its own gold hoarding in 1931. It’s not an entirely novel perspective: Irwin cites contemporary expert warnings of the dangers of French & US conduct even as prices seemed to be stabilising in 1928 and the first half of 1929. What’s new is his finding that world prices would have risen in 1929-33 rather than plunging, had France and the US merely maintained their 1928 ratio of reserve gold to money supply. The associated graph is striking, but not entirely convincing: for one thing, it doesn’t explain falling prices in 1925-28, when French and US gold holdings were reasonably well-behaved and world gold reserves rising broadly in line with economic output; it also doesn’t show what the projected price trend would have been under the same assumptions but with no additional monetary gold from 1928, as was effectively the case. Even with the average world economic growth rate of around 3¾% annually over 1922-29, an absence of extra “active” gold would seem insufficient to account for the scale of the subsequent collapse of prices – and that’s before taking into account the reversal of real output growth in the early 1930s. But it certainly didn’t help.

In fairness to the French, it should be remembered that despite converting a large part of its sterling holdings into gold from 1927, the Banque’s reserves still suffered through Britain’s effective 30% devaluation in 1931. If – as most commentators seem to agree – sterling was indeed overvalued by something like a tenth in 1925, then gold indeed made more sense than at least one of the world’s notional reserve currencies. French gold hoarding of course contributed to sterling’s difficulties, so it’s not much of an excuse. And the franc was itself widely regarded as undervalued from 1928, making the country already a gold sink. Though cushioned to some extent against the first impact of the 1929 global economic downturn, France was to pay dearly for its attachment to gold as she entered the worst phase of the depression just as many countries were starting to climb out of it in 1933: not until 1936 did the country finally free itself of what Keynes had dubbed the gold “fetish”, the last power to do so. By 1938 France’s share of world gold reserves was down from its 1932 peak of 28% to just a tenth.

What are we to make of it all? Well, for one thing proclaiming a new international regime doesn’t make it so without the mechanisms to implement it. Could the gold exchange standard have worked as envisaged at Genoa in 1922? For a time, no doubt, with better alignment of the key currencies and binding undertakings to play the game: supply of the required metal was to prove adequate in the 1930s, as it could have been in the 1920s. But by then it was too late: the inflexibility implicit in the attempt to return to gold and the impossibility of ensuring its optimal distribution had crippled not just the monetary system but the wider economy. Would a more internationally-minded Banque de France have spared the world the nightmare of Depression and war? Possibly not: there was far more amiss in the interwar economy than just monetary policy and gold stocks. France may not have caused the Depression, but it made things a lot worse.

Friday 17 September 2010

De-industrialisation then and now

De-industrialisation is back on the political agenda with the continued erosion of manufacturing employment and GDP share in western economies during the recent economic downturn. US manufacturing employment has fallen by nearly two-fifths from its 1979 peak, standing today at roughly the level of the 1940s despite the intervening doubling of the US population. And the pattern is broadly repeated across the developed world. The UK has seen perhaps the steepest drop, from 9 million in the 1950s and 6.9m in 1979 to a mere 2.5m today.

Shares of current-price GDP overstate (perhaps doubling) manufacturing’s constant-price output decline relative to other sectors because of differing cost and price movements with in the economy. But the pattern is clear enough: for the developed countries as a whole, manufacturing’s share of GDP has halved in the last half-century to around 15%. From an all-time peak of 30% in 1943 and a peacetime high of 28% a decade later, the sector’s share of US GDP has fallen since the late 1960s from a quarter to a mere 11% in 2009. In Britain the proportion has plunged from 37% in 1955 to just 12%. France has seen a less precipitous decline, while Japan and Germany have kept their share above a fifth, down from around a third in the 1960s. The former USSR and eastern Europe experienced their own abrupt fall in the 1990s, coupled with severe drops in real GDP in the early part of the decade.

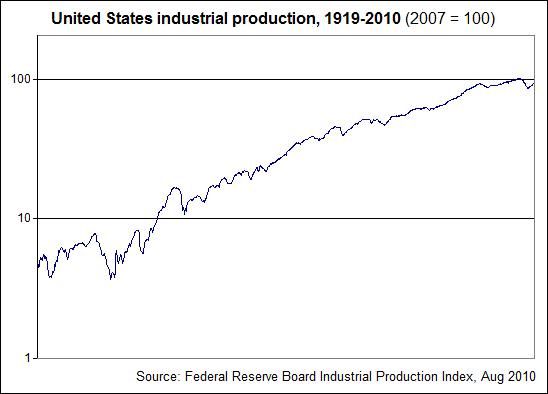

The absolute volume of output has of course shown a quite different trend to employment or GDP share, quintupling in the US since 1953 according to the Federal Reserve’s industrial production index, despite a slowdown from around 1970 and indications of another since 2000. Except in Britain, where output has only doubled, manufacturing in the west as a whole has followed a similar trend, with Europe lagging by a decade or so. But European economies too show signs of the deceleration in manufacturing growth following the high rates of the first postwar decades.

So today’s de-industrialisation is something of a misnomer in terms of output, where until the downturn of 2008 the sector continued to enjoy growth of 20% per decade in most of the older industrial countries. Output decline is – except in some of the worst-affected transition economies – only relative. The sector’s comparative eclipse is in part a manifestation of growing affluence, as an ever larger proportion of our rising spending goes on consumption of services, much as demand for industry’s output surpassed and ultimately dwarfed that for agricultural produce in 1780-1950. In terms of jobs, however, the phenomenon is a very real one for the millions displaced, often in localities heavily dependent on industrial earnings and with limited alternative job opportunities.

But de-industrialisation is itself nothing unique to the past six decades. Today’s shift of the centre of gravity of world industrial activity from richer toward poorer countries is only a reversal of the nineteenth-century trend which saw traditional manufactures driven from mass markets by cheaper factory goods. The difficulties facing older industrial economies today offer striking parallels to those encountered by producers in less developed countries in the earlier period. Problems of erosion of overseas market share and competitors’ encroachment on raw material supply were faced too by Britain in the later 19th century as the country lost its initial dominance in mechanised production, even while its factory output growth averaged 2¼% a year.

The scale of manufacturing production before modern industrialisation is notoriously difficult to gauge, even in more developed countries. Official returns until the 1950s tended to measure the output only of factories and workshops exceeding a given number of workers or value of output – sufficient to indicate 20th-century growth in industrial countries, but a poor guide to the pattern in traditional ones where manufacture tended to be more dispersed among small producers. Isolated estimates exist for parts of pre-industrial Europe, and even for regions of 19th-century India before the advent of modern census-taking. For England, we have reworkings of Gregory King’s calculations indicating nearly £8m of manufacturing value added in 1688 (more than £1.4 per head or nearly a sixth of national income), showing a country already in advance of most of its competitors. Recent research on occupational distributions has supported the existence of large “pre-industrial” industrial populations. But global manufacturing volume before the past half-century or so has remained a largely overlooked topic, with one notable exception.

Before we had Angus Maddison’s historical GDP estimates, there were Paul Bairoch’s figures for manufacturing output for the world and principal producing regions & countries for the period 1750-1980. Whenever you encounter a statement to the effect that 18th-century China produced a third of the world’s manufactures or India a quarter, it’s from Bairoch. Like Maddison’s data, Bairoch’s have become so embedded in discussion of long-run economic growth that they’re routinely cited with no indication that they might be anything but 100% accurate, and sometimes without even any identification of the source: to many they simply are “the” numbers.

In fact Bairoch has come in for considerable scholarly criticism over the years, not least for vague indication of sources and for guesstimating output levels before modern industrialisation. But his actual estimates have never been overturned: on the contrary, his finding of massive de-industrialisation in less developed countries has received indirect support from Maddison’s GDP data and more recently from Pomeranz’s finding of an 18th-century Chinese economy quantitatively not dissimilar to Europe’s: Maddison’s figures indeed indicate (rather implausibly) a Chinese economy larger (though of course far poorer in per capita terms) than that of the US as late as 1888.

Bairoch took a very different approach to Maddison (at least in theory), rejecting projection into the past of apparent growth rates as an unreliable indicator of early output levels. Instead he guesstimated plausible consumption of manufactures in pre-industrial societies, adding subsequent factory production and making a deduction for the part of traditional output supplanted by imports. In practice, Maddison has of course spliced similar benchmark observations into his GDP growth series for points far from his notional 1990 benchmark, hence the substantial compatibility of the two sets of data.

The first thing to be said of Bairoch’s “pre-industrial” numbers is, like Maddison’s for China and India, they’re big. Bairoch was sufficiently aware of the enormous pricing pitfalls in valuing output over time to limit his results to a volume index based on the UK’s 1900 level of manufacturing output. But since we know the approximate value of British manufacture in 1900 (and can indeed fairly reliably estimate that year’s global manufacturing value on the basis of existing national accounts calculations) we can value his global estimate for 1700 at roughly $5bn of gross output at 1900 prices – a vast quantity implying perhaps $2¼bn of value added, around a seventh of total world product and indeed little smaller a proportion than in 1900.

The focus of Bairoch’s work is however not so much the global trend but the geographical distribution of manufacturing activity. Here his conclusions are startling: Chinese output exceeded the whole of continental Europe’s (including Russia but excluding Britain) as late as 1830, while India produced nearly as much as Britain, France and Germany combined. The west’s subsequent de-industrialisation impact on Asia was still more startling: Indian output of manufactures fell by 73% in 1830-80, China’s less abruptly – by 39% over 1830-1913 - but by a similar absolute volume exceeding a billion dollars in annual gross value. Overall the non-European world (excluding Japan) lost some 47% of its manufacturing capacity, its share of world output plunging from 73% in 1750 to a mere 7% two centuries later.

It’s a shocking picture, but one resting on uncertain foundations. Taking the classic case of 19th-century de-industrialisation – India’s traditional cotton industry – it seems that while handspinning production indeed followed the course outlined by Bairoch’s data, its decline was partly offset by the expansion of mill output in the second half of the century, while the sector’s weaving branch fared better. Millions still lost their livelihoods and the country was for a time reduced from a leading world exporter to an industrial backwater as industrialisation took off elsewhere, but there is no evidence for quite the scale of output collapse portrayed in Bairoch’s estimates. Albert Feuerwerker has found a similar pattern in China, where his calculations indicate that traditional weaving grew slightly over 1870-1910 on the strength of mill yarn imports. Nor was this a distinctly Asian phenomenon: numbers in English handloom weaving had likewise risen in the early 19th century even as handspinning was becoming a thing of the past.

Textile products represent only a fraction of manufacturing. But in the first decades of the 19th century they represented the most dynamic sector in the transition to mechanised factory industry, accounting for half of British exports in 1830. If any traditional industry faced oblivion at the hands of British and later western European and US competition, it was handicraft cotton manufacture. The implication is that Bairoch overstates both Asian manufacturing output in the 18th and early 19th centuries and the scale of its decline from 1830. His other figures are, however, broadly of the right order of magnitude, and illustrate the retreat of traditional production not just at regional but at global level, from perhaps an eighth of global value added in 1700 to a mere 3-4% two centuries later.

And de-industrialisation has a history even older than the era of the industrial revolution. Gregory Clark finds evidence of relative decline in non-agricultural employment in areas of rural East Anglia as early as the 14th-16th centuries:

While only 39 percent of the employed in these parishes were in farming in 1381, by some of the decades in the early seventeenth century this share had risen to nearly 70 percent. Rural Suffolk was more “industrialized” in 1381 than in any years observable 1550-1700 up till 1831. Rural Suffolk seems to have experienced “de-industrialization” between 1381 and 1600.The story is repeated across early-modern France, Germany, Iberia and Italy, as new manufacturing districts arose to supplant rural crafts, or as competition from regions with more direct access to the centres of the new Atlantic economy brought a wholesale shift to the north and west.

De-industrialisation has been with us for many centuries. What’s new is the rapidity and scale of the downturn in manufacturing employment in parts of the western world over recent decades. History offers no miracle cures: few will want to emulate the “sink or swim” laissez-faire approach which saw the permanent loss of a quarter of Britain’s manufacturing jobs in 1979-83 alone, but protecting or shoring up declining industries has usually tended only to postpone eclipse in the absence of ongoing active promotion of research, modernisation and expertise. Britain’s 20th-century experience should serve as a warning against complacency and reliance on compliant markets: in the 21st there may be no place for rich countries’ products without constant effort to maximise the skills, innovation and creativity that gave them their initial lead.

Wednesday 8 September 2010

Trading myths

Discussions of past world trade abound with widely diverging calculations, surely enough to have estimators of GDP congratulating each other on the closeness of their findings.

According to Kenwood & Lougheed (The growth of the international economy, 1971),

The authors were referring to total foreign trade, in other words the combined figure for exports plus imports. Since this totalled around $40bn in 1913, their implied world product works out at roughly $120bn. And as world population had nearly doubled in the meantime, their estimate implies for 1800 a world product approaching $28bn and trade totalling $0.8bn at 1913 prices.

In 1995 Angus Maddison came up with a far lower ratio for 1913 of 8.7% of GWP for exports alone, which he lowered still further in 2001 to 7.9%, up from 1% in 1820 and 4.6% (originally 5%) in 1870. Since he also estimated current-price exports at $18.4bn in 1913 and $5.1bn in 1870, this implies a gross world product of $230bn in 1913 and $110bn in 1870, when prices were rather higher before the onset of the “great depression”. However, his ratios are computed at 1990 prices, which as we’ve seen aren’t necessarily the best guide even to the first half of the 20th century, let alone the 19th. Maddison offers no current-price figure for exports in 1820, but his volume estimate broadly agrees with Mulhall’s sterling value for total world trade in suggesting around $0.8bn - a value that is difficult to reconcile with Maddison’s 1% share of GDP, even given the eccentricities of 1990 Geary-Khamis dollar projections and the high prices of the 19th century’s opening decades.

Maddison’s estimates have become the standard in much of the literature, notably in recent work by Kevin O’Rourke, Jeffrey Williamson and Alan Taylor, who use them to show that exports grew more rapidly relative to GWP before 1913 than since. But are they reliable? The answer depends on what we’re measuring. As independent projections of two distinct variables from a 1990 base they may each possess some validity. But whether the resulting ratio corresponds to reality is another matter.

Fortunately a check is available, in the form of current-price data for leading countries and estimates of world trade at both current and constant prices from the 1870s. To take the most obvious case, the exports of Britain - the leading trading nation of the 19th century - are put by Maddison at 3.1% of GDP in 1820 and 12.2% in 1870. But at the prices of the time, the proportion (excluding re-exports of £10m and £45m) rose from around 9% to a fifth. For the US, exports reached 3.7% of GDP in 1913 according to Maddison’s series, but at that year’s prices were around 6½%: the corresponding ratio for Germany is likewise understated by upwards of a fifth, for France by half; China fares still worse, even reckoning GDP at the most generous level compatible with likely output.

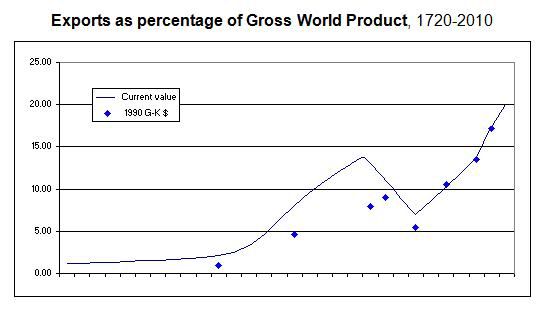

Mulhall’s trade data on the other hand appear consistent both with Maddison’s current-price data and with the British returns extending back through the 18th century. His figures include Britain’s large re-export trade and presumably the transit trade of the Netherlands whose inclusion as undifferentiated exports irked 20th-century international statisticians, but they can be adjusted for both. He also combines imports and exports, so his totals need reducing by more than half to omit not only the double-counted merchandise but also freight & insurance costs. Expressed as a percentage of current-price world product, the results were combined with post-1870 data to yield the following decennial series (except 1913, 1929 and 1937):

The current-price estimates indicate that the 1990 G-K dollar data grossly understate exports relative to GDP in 1820, 1870 and 1913. The 1% level was probably reached around 1700 rather than 1820, when the real ratio was about 2%. The 1870 ratio similarly already exceeds Maddison’s 7.9% for 1913, when the true figure reached 13%. The discrepancy extends to 1950, for which Maddison inexplicably reduced his already somewhat low 7% to a calamitous 5½%.

Kenwood & Lougheed on the other hand seem to have been remarkably accurate all those years ago with their estimate of world output in 1800 (assuming that they started from accurate trade & population figures for 1913), though they underestimated both trade in the earlier year and GWP in the second. The intervening rise in the export ratio was not elevenfold but probably slightly less than eightfold.

While Mulhall's early estimates doubtless contain an element of approximation, this is not sufficient to greatly alter the conclusion, and there is no indication that he overstated "unknowns": if anything, non-western countries' share looks likely to be understated. Furthermore, the finding of far larger early-modern trade is supported by still earlier estimates such as Braudel's astonishing tenth of national income (upwards of 0.4% of world product) for 16th-century French imports (a good part doubtless for re-export).

One peculiarity of the Maddison series is its suggestion that exports outstripped world output in 1913-29, a notion which would have surprised contemporary experts: in fact at current prices the 1913 percentage was not surpassed until the 1973 oil price rise raised the total to $850bn - a still more shocking finding that calls for future investigation but which in view of postwar western liberalisation would seem to reflect faster intervening growth in services and in output of less trade-dependent regions more than policy or failure of the trading system.

In terms of volume, the data illustrate four familiar stages of export growth over the past 300 years: an annual increase of about 1% to c.1815, an acceleration to 3½% in the following century and then a period of near-stagnation from 1914 until the resumption of rapid growth from the mere $37bn of 1946, leading to the 5-6% annual increases of recent decades. Comparison of the century to 1913 with the one after is uninstructive as the second comprises three decades which form part of neither suggested period of globalisation: of these, the last showed faster growth, but the earlier trade surge produced a sevenfold rise in exports’ share of gross product.

On a speculative note, compared to Maddison's more linear 1820-1929 trend, the slowing of export growth from the high rates of 1830-60 lends the current-price estimates the appearance of a flattened S-curve interrupted in 1914 and with which the subsequently disrupted export/GDP ratio is only now once again intersecting as it approaches the former's implied upper bound of perhaps 30%. The slowdown of 1861-1913 of course owes much to the successive impacts of the US Civil War, the 1873-96 price depression and the rise of protection, but each of these in its own way reflects trade-related stresses suggestive of a finite tolerance for commercial openness at the aggregate global level. Much has of course changed in the intervening century, but it remains to be seen whether the 21st century resumes the trend of the 19th or continues that of the late 20th.

It seems clear that in real terms international merchandise trade was more significant in the early 19th century than the currently-accepted estimates allow for. That still means that nearly 98% of output supplied domestic demand in 1820, 99% in 1700. But the world was already a little more “global” than we’ve been led to believe, and was to remain so into the comparatively recent past. The resulting flattened growth trend may be indicative of future limits to trade globalisation, or of an ongoing structural break with past centuries.

According to Kenwood & Lougheed (The growth of the international economy, 1971),

By 1913, the volume of foreign trade per capita had grown to over 25 times what it had been in 1800, whereas world output per head had grown only 2.2 times over the same period. This means that during the period 1800-1913 the foreign trade proportion, that is, the ration of world trade to world product, rose to over 11 times its initial level. Moreover, if, as seems likely, the world proportion of foreign trade to product was about 33 per cent in 1913, it must have been barely 3 per cent in 1800.

The authors were referring to total foreign trade, in other words the combined figure for exports plus imports. Since this totalled around $40bn in 1913, their implied world product works out at roughly $120bn. And as world population had nearly doubled in the meantime, their estimate implies for 1800 a world product approaching $28bn and trade totalling $0.8bn at 1913 prices.

In 1995 Angus Maddison came up with a far lower ratio for 1913 of 8.7% of GWP for exports alone, which he lowered still further in 2001 to 7.9%, up from 1% in 1820 and 4.6% (originally 5%) in 1870. Since he also estimated current-price exports at $18.4bn in 1913 and $5.1bn in 1870, this implies a gross world product of $230bn in 1913 and $110bn in 1870, when prices were rather higher before the onset of the “great depression”. However, his ratios are computed at 1990 prices, which as we’ve seen aren’t necessarily the best guide even to the first half of the 20th century, let alone the 19th. Maddison offers no current-price figure for exports in 1820, but his volume estimate broadly agrees with Mulhall’s sterling value for total world trade in suggesting around $0.8bn - a value that is difficult to reconcile with Maddison’s 1% share of GDP, even given the eccentricities of 1990 Geary-Khamis dollar projections and the high prices of the 19th century’s opening decades.

Maddison’s estimates have become the standard in much of the literature, notably in recent work by Kevin O’Rourke, Jeffrey Williamson and Alan Taylor, who use them to show that exports grew more rapidly relative to GWP before 1913 than since. But are they reliable? The answer depends on what we’re measuring. As independent projections of two distinct variables from a 1990 base they may each possess some validity. But whether the resulting ratio corresponds to reality is another matter.

Fortunately a check is available, in the form of current-price data for leading countries and estimates of world trade at both current and constant prices from the 1870s. To take the most obvious case, the exports of Britain - the leading trading nation of the 19th century - are put by Maddison at 3.1% of GDP in 1820 and 12.2% in 1870. But at the prices of the time, the proportion (excluding re-exports of £10m and £45m) rose from around 9% to a fifth. For the US, exports reached 3.7% of GDP in 1913 according to Maddison’s series, but at that year’s prices were around 6½%: the corresponding ratio for Germany is likewise understated by upwards of a fifth, for France by half; China fares still worse, even reckoning GDP at the most generous level compatible with likely output.

Mulhall’s trade data on the other hand appear consistent both with Maddison’s current-price data and with the British returns extending back through the 18th century. His figures include Britain’s large re-export trade and presumably the transit trade of the Netherlands whose inclusion as undifferentiated exports irked 20th-century international statisticians, but they can be adjusted for both. He also combines imports and exports, so his totals need reducing by more than half to omit not only the double-counted merchandise but also freight & insurance costs. Expressed as a percentage of current-price world product, the results were combined with post-1870 data to yield the following decennial series (except 1913, 1929 and 1937):

The current-price estimates indicate that the 1990 G-K dollar data grossly understate exports relative to GDP in 1820, 1870 and 1913. The 1% level was probably reached around 1700 rather than 1820, when the real ratio was about 2%. The 1870 ratio similarly already exceeds Maddison’s 7.9% for 1913, when the true figure reached 13%. The discrepancy extends to 1950, for which Maddison inexplicably reduced his already somewhat low 7% to a calamitous 5½%.

Kenwood & Lougheed on the other hand seem to have been remarkably accurate all those years ago with their estimate of world output in 1800 (assuming that they started from accurate trade & population figures for 1913), though they underestimated both trade in the earlier year and GWP in the second. The intervening rise in the export ratio was not elevenfold but probably slightly less than eightfold.

While Mulhall's early estimates doubtless contain an element of approximation, this is not sufficient to greatly alter the conclusion, and there is no indication that he overstated "unknowns": if anything, non-western countries' share looks likely to be understated. Furthermore, the finding of far larger early-modern trade is supported by still earlier estimates such as Braudel's astonishing tenth of national income (upwards of 0.4% of world product) for 16th-century French imports (a good part doubtless for re-export).

One peculiarity of the Maddison series is its suggestion that exports outstripped world output in 1913-29, a notion which would have surprised contemporary experts: in fact at current prices the 1913 percentage was not surpassed until the 1973 oil price rise raised the total to $850bn - a still more shocking finding that calls for future investigation but which in view of postwar western liberalisation would seem to reflect faster intervening growth in services and in output of less trade-dependent regions more than policy or failure of the trading system.

In terms of volume, the data illustrate four familiar stages of export growth over the past 300 years: an annual increase of about 1% to c.1815, an acceleration to 3½% in the following century and then a period of near-stagnation from 1914 until the resumption of rapid growth from the mere $37bn of 1946, leading to the 5-6% annual increases of recent decades. Comparison of the century to 1913 with the one after is uninstructive as the second comprises three decades which form part of neither suggested period of globalisation: of these, the last showed faster growth, but the earlier trade surge produced a sevenfold rise in exports’ share of gross product.

On a speculative note, compared to Maddison's more linear 1820-1929 trend, the slowing of export growth from the high rates of 1830-60 lends the current-price estimates the appearance of a flattened S-curve interrupted in 1914 and with which the subsequently disrupted export/GDP ratio is only now once again intersecting as it approaches the former's implied upper bound of perhaps 30%. The slowdown of 1861-1913 of course owes much to the successive impacts of the US Civil War, the 1873-96 price depression and the rise of protection, but each of these in its own way reflects trade-related stresses suggestive of a finite tolerance for commercial openness at the aggregate global level. Much has of course changed in the intervening century, but it remains to be seen whether the 21st century resumes the trend of the 19th or continues that of the late 20th.

It seems clear that in real terms international merchandise trade was more significant in the early 19th century than the currently-accepted estimates allow for. That still means that nearly 98% of output supplied domestic demand in 1820, 99% in 1700. But the world was already a little more “global” than we’ve been led to believe, and was to remain so into the comparatively recent past. The resulting flattened growth trend may be indicative of future limits to trade globalisation, or of an ongoing structural break with past centuries.

Monday 6 September 2010

1946 & all that

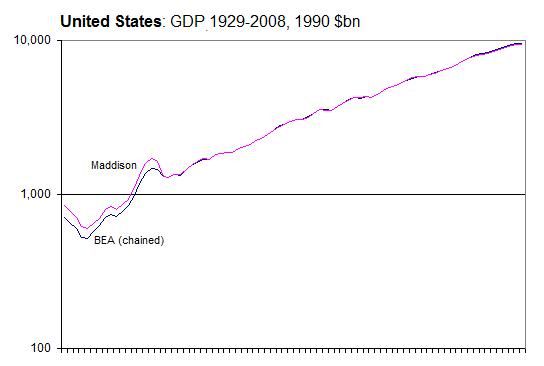

It was the last year of global economic contraction, as countries struggled to overcome wartime destruction & dislocation and postwar political strife, avert international food crisis and reconvert from military to peacetime production. For the United States, 1946 saw an exceptionally severe drop in real output as the nation dismantled its vast war apparatus and sought to return once again to "normalcy". Indeed while the rest of the world experienced little net change, Angus Maddison's data - widely used as the standard in historical GDP comparison - show real US GDP falling by more than a fifth, the sharpest annual downturn since records began.

That US economic activity fell sharply in real terms in 1945-46 is beyond question. Industrial output was down as early as April 1945 as the war in Europe neared its end. With Japan's surrender, the War Department cancelled contracts worth nearly $23 billion in August alone, and 2.5 million workers were released from war jobs in the first month of peace. The industrial downturn continued into 1946, and the peak wartime level of manufacturing activity was not reattained until 1950, a reflection of the scale of the country's earlier economic mobilisation.

What's at issue is the extent of the drop, both in the US and globally. Maddison's data show the 1990 Geary-Khamis dollar value of US GDP falling from 1.64 trillion in 1945 to little over 1.3trn in 1946. And this decline represents 7% of gross world product in 1945, enough to turn an otherwise small further decline from that year's already greatly reduced aggregate global output into a massive postwar world contraction.

But today's official US historical National Income & Product Accounts show no such calamitous plunge in the first year of peace. The answer comes from the Bureau of Economic Analysis, which in 1996 replaced its fixed-price real GDP estimates with chained indexes incorporating year-on-year price changes. The May 1997 Survey of Current Business explains:

Maddison's GDP trend thus corresponds closely to the BEA series abandoned in 1996, with a base-year shift from 1987 to 1990. The effects are significant: in today's chained series, the GDP of 1945 was not equalled until 1950; according to Maddison, this didn't happen until 1953. The higher 1944 wartime peak was surpassed only in 1951 according to the BEA, but in Maddison's series the 1953-54 recession meant this took until 1955.

Nor is the impact in Maddison's data of merely national sugnificance: his series indicates a 7% fall in world output in 1946 alone, equalling that of the previous year when the ending of Allied war production combined with the devastation of German and Japanese industry & infrastructure. Replacing his US trend with the BEA's, however, the global drop is about 3% - far smaller than that of 1945, as we might expect given the ending of the world's largest and most destructive armed conflict.

And the effect isn't limited to the period of victory and postwar adjustment & overseas reconstruction. For Maddison's trend before 1946 broadly coincides with the BEA's. If the chained US series is correct, Maddison's 1929-45 US data are overstated by 10-20% or more relative to those that follow - and the discrepancy widens toward the beginning of the period covered by both sets. Which is doubly problematical, because there's good reason to believe that his figures for earlier years already understate the real US share of GWP.

The current-price data certainly support the chained series as a more appropriate representation of reality. Current-price GDP was virtually unchanged in 1946 (from $223bn to $222.1bn). Durable-goods manufacture was down sharply, almost entirely down to the plunge in output of ships & vehicles; government's share was down by an even greater amount as millions settled back into civilian life. But consumer-goods production was up, as were retail & wholesale trade, construction and services.

Prices were certainly up substantially with the lifting of wartime controls, a trend which would continue in 1947 and 1948. But the scale of Maddison's real-GDP downturn would require a rise of more than a quarter in the unit value of net output. It just isn't there. Consumer price inflation picked up sharply in the second half of 1946, but for the year as a whole averaged little over 8%. Commodity prices rose more strongly, but their greatest increase would come in 1947. The BEA's GDP deflator shows only a 12% rise, the same as that implied by the old 1947-price data. Real GDP therefore fell by 11%, again in line with the 1947 series.

Maddison himself was aware of the issue, admitting candidly that his preference for the 1987/90-price version derived in large part from his doubting a near-doubling of real US GDP in 1937-50. It's an enormous rise, but less daunting when we recall that per capita income in 1937 was still below the level of 1926, and that both his and the chained series indeed show such a doubling for the still briefer period 1937-44. The alternative of a real 25% drop in 1944-47 requires a far greater leap of faith.

If Maddison's 1870-1945 estimates of US GDP are misleading, his world totals cannot but be affected given the size of the US economy even in the late 19th century. Lowering them to conform to his 1946-2008 figures would however indicate an unrealistically low US share of a mere sixth of world output in 1913, when current-price data suggest something nearer to a quarter than Maddison's raw 19%. Adjusting the US series necessitates correcting the data for other parts of the world, some of which already appear overstated.

The 1946 problem should remind us that 1990 G-K dollars can be an unreliable guide in estimating historical GDP. The pricing issues can too easily leave us with implausible trends or relative volumes of output. The Maddison dataset and extrapolations from it should be used with great caution until we can come up with something better.

That US economic activity fell sharply in real terms in 1945-46 is beyond question. Industrial output was down as early as April 1945 as the war in Europe neared its end. With Japan's surrender, the War Department cancelled contracts worth nearly $23 billion in August alone, and 2.5 million workers were released from war jobs in the first month of peace. The industrial downturn continued into 1946, and the peak wartime level of manufacturing activity was not reattained until 1950, a reflection of the scale of the country's earlier economic mobilisation.

What's at issue is the extent of the drop, both in the US and globally. Maddison's data show the 1990 Geary-Khamis dollar value of US GDP falling from 1.64 trillion in 1945 to little over 1.3trn in 1946. And this decline represents 7% of gross world product in 1945, enough to turn an otherwise small further decline from that year's already greatly reduced aggregate global output into a massive postwar world contraction.

But today's official US historical National Income & Product Accounts show no such calamitous plunge in the first year of peace. The answer comes from the Bureau of Economic Analysis, which in 1996 replaced its fixed-price real GDP estimates with chained indexes incorporating year-on-year price changes. The May 1997 Survey of Current Business explains:

As measured by the old 1987 fixed-weighted index, real GDP dropped 25 percent from 1944 to 1947, reflecting the post-World War II demobilization and the associated sharp cutbacks in defense spending. However, much of this drop reflects the use of 1987 prices for defense equipment rather than the low postwar prices for defense equipment. As measured by the more appropriate price weights of BEA's new chain-type indexes, the postwar drop in real GDP is 13 percent.

Maddison's GDP trend thus corresponds closely to the BEA series abandoned in 1996, with a base-year shift from 1987 to 1990. The effects are significant: in today's chained series, the GDP of 1945 was not equalled until 1950; according to Maddison, this didn't happen until 1953. The higher 1944 wartime peak was surpassed only in 1951 according to the BEA, but in Maddison's series the 1953-54 recession meant this took until 1955.

Nor is the impact in Maddison's data of merely national sugnificance: his series indicates a 7% fall in world output in 1946 alone, equalling that of the previous year when the ending of Allied war production combined with the devastation of German and Japanese industry & infrastructure. Replacing his US trend with the BEA's, however, the global drop is about 3% - far smaller than that of 1945, as we might expect given the ending of the world's largest and most destructive armed conflict.

And the effect isn't limited to the period of victory and postwar adjustment & overseas reconstruction. For Maddison's trend before 1946 broadly coincides with the BEA's. If the chained US series is correct, Maddison's 1929-45 US data are overstated by 10-20% or more relative to those that follow - and the discrepancy widens toward the beginning of the period covered by both sets. Which is doubly problematical, because there's good reason to believe that his figures for earlier years already understate the real US share of GWP.

The current-price data certainly support the chained series as a more appropriate representation of reality. Current-price GDP was virtually unchanged in 1946 (from $223bn to $222.1bn). Durable-goods manufacture was down sharply, almost entirely down to the plunge in output of ships & vehicles; government's share was down by an even greater amount as millions settled back into civilian life. But consumer-goods production was up, as were retail & wholesale trade, construction and services.

Prices were certainly up substantially with the lifting of wartime controls, a trend which would continue in 1947 and 1948. But the scale of Maddison's real-GDP downturn would require a rise of more than a quarter in the unit value of net output. It just isn't there. Consumer price inflation picked up sharply in the second half of 1946, but for the year as a whole averaged little over 8%. Commodity prices rose more strongly, but their greatest increase would come in 1947. The BEA's GDP deflator shows only a 12% rise, the same as that implied by the old 1947-price data. Real GDP therefore fell by 11%, again in line with the 1947 series.

Maddison himself was aware of the issue, admitting candidly that his preference for the 1987/90-price version derived in large part from his doubting a near-doubling of real US GDP in 1937-50. It's an enormous rise, but less daunting when we recall that per capita income in 1937 was still below the level of 1926, and that both his and the chained series indeed show such a doubling for the still briefer period 1937-44. The alternative of a real 25% drop in 1944-47 requires a far greater leap of faith.

If Maddison's 1870-1945 estimates of US GDP are misleading, his world totals cannot but be affected given the size of the US economy even in the late 19th century. Lowering them to conform to his 1946-2008 figures would however indicate an unrealistically low US share of a mere sixth of world output in 1913, when current-price data suggest something nearer to a quarter than Maddison's raw 19%. Adjusting the US series necessitates correcting the data for other parts of the world, some of which already appear overstated.

The 1946 problem should remind us that 1990 G-K dollars can be an unreliable guide in estimating historical GDP. The pricing issues can too easily leave us with implausible trends or relative volumes of output. The Maddison dataset and extrapolations from it should be used with great caution until we can come up with something better.

Sunday 5 September 2010

Counting the English

Excitement abounds in the Chiffrephile household at the arrival of the latest in Stephen Broadberry et al's long-run quantitative reassessments of medieval and modern Britain. This time Bruce Campbell and Bas van Leeuwen complete the authorship for English medieval population, spanning the 11th-16th centuries.

Besides the obvious benchmarks of Domesday Book, the 1377 Poll Tax record and the start of Wrigley & Schofield's 330-year demographic reconstruction in 1541, the work follows from (though to some extent retreats from) Campbell's skilful demolition of the absurdly high peak 14th-century estimate of six million or more in vogue since it was suggested (initially as a speculative aside) by Michael Postan nearly half a century ago.

As far back as 1996 Campbell and Mark Overton demonstrated that English agriculture at its medieval peak c.1300 was likely to have fed only some 4-4.5 million people (and probably nearer the lower end of the range), revised by Campbell four years later to 4.38m: this time the authors have settled on a less rigorous 4.81m, which they admit is close to the maximum attainable. The concession derives from their needless timidity in dispatching the weakest of Postan's propositions:

Whereas Russell assumed that children under the age of 15 accounted for 33.3 percent of the population, Postan suggested that the ratio may have been as high as 40 to 45 per cent. For the period after 1541, when reliable data become available, the percentage of under-15s in the population never rose above 40 percent, which surely represents the upper limit for 1377. As Blanchard points out, such a high ratio tended to occur in periods of rapid population growth driven by high fertility. Since population was declining in the aftermath of the Black Death, a ratio as high as 40 to 45 per cent in the 1370s is improbable and a lower ratio more likely.

In fact Postan's 40-45% claim is quite preposterous and underlines the fragility of his whole speculation: there's plenty of evidence from populations with similar mortality and growth rates to indicate that anything much outside the 30-35% range is most unlikely for the under-14's (not under-15's) excluded from the tax's coverage: indeed given what we know of medieval mortality, to find 40-45% so aged we'd have to be looking at 2% annual growth, about six times the average for the 12th-13th centuries. The much-maligned Russell was spot-on on this count, for all his strange notions of 14th-century household size.

Since our estimates for the decades before the Black Death are founded on projecting back from 1377 with an allowance for the extraordinary intervening mortality (traditionally taken to be in the region of 40%, but raised in the Postan conjecture to 50% with no apparent allowance for the likely elevated birth rate between epidemics), the higher 1377 total means more people in 1348 than might otherwise be the case. Correcting the under-14 allowance to Russell's third offers a better fit with the agricultural carrying-capacity approach.

Postan was on stronger ground with his suggestion that omissions were far higher in 1377 than the 5% allowed for by Russell (indeed few now take Russell's rate seriously, comparing favourably as it does to many modern censuses). The authors err however in adopting his proposed 25% as a likely maximum for omissions in an earlier and quite different enumeration:

Although Harvey did not present any underlying calculations, she claimed that the Domesday population could well have approached 2 million. Rather than arguing for a higher household multiplier, Harvey argued for a much greater scale of omissions than the 5 per cent allowance made by Darby (1977), on the grounds that Domesday Book was more concerned with the landed wealth of the tenants-in-chief and their head tenants, and hence tended to under-record or omit the small-holding and landless elements. The final column of Table 1 presents an estimate of the English population in 1086 in the spirit of Harvey’s assumptions. This involves increasing the rate of omissions from 5 per cent to 25 per cent — the maximal scale of omissions claimed by Postan for the Poll Tax of 1377 — which results in a population of 1.87 million. Note that for the population to exceed 2 million, which Harvey claims should not be ruled out, would require an omissions rate of the order of 40 per cent.

The bulk of the omissions suggested by Harvey are, however, of a quite different character to those postulated for 1377. In 1086 the issue is not merely of oversights and evasions but of whole strata of the population being left out of the count because they were (quite correctly) deemed irrelevant to its purpose and therefore not worth recording. The number unrecorded will never be known precisely because they were left out, but the proportion could quite possibly have reached the higher level with no implication of similarly massive understatement in 1377.

So what of the final series? The figures are realistic, though by erring toward the mainstream, they may understate the level at the start (1086) and more likely overstate it in the middle (1290-1377). Interestingly, the authors find for 1348 on the great 14th-century peak population question, with the rival contender 1315 mustering only 4.69m, already down from 4.75m in 1290. Their estimate of a 12% fall in 1315-25 sheds new light on the disastrous results of the great famine of the early part of the decade and the harvest & livestock losses of later years.

The county estimates and maps toward the end of the paper offer further insight, even if they derive from already published distributions adjusted for the new totals: the striking growth of Lancashire's share in the period before 1600 should alone gladden the heart of those who see continuity where others see abrupt breaks.

All in all, it's a rewarding paper: apart from their over-hasty dismissal of Harvey's Domesday speculation, the authors may take sufficient confidence in their gut instincts to adopt a slightly more bare-knuckle approach in the inevitable revisions.

Saturday 4 September 2010

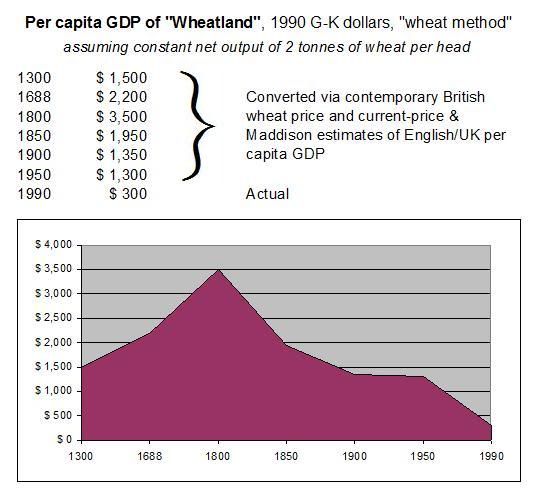

A mess in Mesopotamia

Imagine my excitement at coming across a new estimate for ancient Mesopotamian GDP by the estimable Peter Foldvari and Bas van Leeuwen! Imagine my disappointment at finding my enthusiasm on the wane by the end of paragraph 2!

The paper is essentially an extension to roughly the area of today's Iraq of Elio Lo Cascio and Paolo Malanima's 2009 critique of Angus Maddison's 2003 estimate of per capita GDP (in 1990 dollars) in the Roman Empire by way of the England of 1688. Confused? It gets worse.

The tortured calculations that follow are ultimately down to Maddison, who used Gregory King's estimate of 17th-century English national income as a half-way house in estimating the ratio between modern GDP levels and those of ancient societies. The latter, he concluded, had per capita incomes of around $500, about two-fifths of a 1688 English average equivalent to two tons of wheat.

Lo Cascio & Malanima challenged Maddison's use of average cereal (rather than specifically wheat) prices in the calculation and his reliance on the exceptionally low prices of 1688. England's true wheat-equivalent income, they argued, was nearer 1.2 tons per head - no better than Roman Italy's and less than 50% above that of the Roman Empire generally. Income growth in Europe was thus virtually non-existent over the intervening 1,674 years: other areas of Europe were far behind Italy in Roman times, just as they were far behind England in 1688. So European prosperity may have sagged and revived in the interim, but the net effect was minimal.

In converting Maddison's 1688 grain price denominator to 1676-1700 wheat prices, however, LCM omit to adjust English GDP - the numerator - for the higher 25-year general price level consistant with their revised wheat value. Nor, after questioning Maddison's assumption that Italian GDP per head was 52% higher than the rest of the Empire - whose inhabitants, we are told, could only afford 790kg of wheat - do they incorporate their alternative suggestions of a lower peninsular level. Italian average income may have approached the later English level in terms of wheat: it may equally have been 20-25% lower.

Foldvari & van Leeuwen incorporate LCM's reworking in their approach. What follows is largely guesswork founded on Makis Aperghis's estimate of the value of agricultural production - here rounded from 7,500-10,500 to 10,000 talents, from which the authors deduct a similarly vague fifth for intermediate inputs ("based on the 1841 input-output table for England", we're assured) before adding a conservative 40% to what remains, arriving thereby at a per capita GDP equivalent to 1,077 litres of barley annually, which they then equate to 862 litres of wheat, 52% of English income in 1688 and hence $736 of the 1990 Geary-Khamis dollars used by Maddison.

The issue here isn't so much the final number, which is probably about as useful and relevant as any given that ancient Mesopotamians didn't use 1990 dollars or prices: rather, the method itself exposes the severe shortcomings of the whole approach. For as Foldvari & van Leeuwen observe, the figures imply "an exchange rate of 1.17 litre wheat per one G-K 1990 dollar". This works out at just over 1,100 notional international dollars of 1990 value for a tonne of wheat (and note that the English prices around which the calculation revolves are wholesale, not retail, while the Roman and Mesopotamian levels are computed by bulk rather than value).

The problem is that a tonne of wheat wasn't worth anything approaching $1,100 in 1990. Anywhere. In fact the crop in that year fetched only $135 on the international market. It's true that wheat prices were depressed in the latter part of 1990 following a bumper harvest in the US (where the price was as low as $96). But even at the higher price of 1989 the product was worth only $170 per tonne - rather more than its average of $160 over the whole of 1980-2010, a period that includes the record prices of 2007-08.

Imagine an economy which produced only two tonnes of wheat per head of population (net of seed and that part of the crop traded for other related inputs) and nothing else, trading its resulting healthy grain surplus with visiting foreign merchants for life's other necessities and occasional luxuries. In 1688 this notional territory would enjoy a world-leading per capita GDP of 2,200 G-K 1990 dollars according to the Maddison-LCM-FvL calculations. In the real 1990, however, its inhabitants would earn around $270, in 1989 $340 - below Maddison's subsistence allowance and the dollar-a-day of purchasing power often used to denote crushing poverty, and below even the $434 for Chad, the country at the bottom of Maddison's ranking.

The way current GDP estimates in Geary-Khamis dollars are computed means that the result offers no guide to the value of any product or sector within the economy, nor is it meant to. And the consequent uncertainties multiply as current incomes are projected into the past on the basis of assumed national economic growth rates. But in the aggregate, the final totals are assumed to bear some relation to reality across time and place. The England-Rome-Mesopotamia conjecture shows that they may not.

Friday 3 September 2010

Moritz Schularick gets GWP right

Full marks to Moritz Schularick, who gets pre-WW1 world GDP spot-on - in a paper that isn't even about GDP!

Schularick's implied $140 bn for current-price GWP in 1914 is the best published estimate I've seen, and offers a valuable warning of the shortcomings of projection from today's PPP-adjusted income levels. It's unfortunate that more historians don't adopt a similar approach of calculating current-price values from current-price data rather than recycling dubious estimates based on uncertain growth rates, questionable deflators and anachronistic aggregates.

[Maddison’s] method... yields a historical world GDP of about 210 billion US dollars on the eve of WW1. This would bring the level of international financial integration (the ratio of gross international assets to world GDP in 1913) to around 20% (Crafts, 2000; Obstfeld and Taylor, 2003a). However, a simple comparison of historical GDP reconstruction with the deflated figures indicates that the market value of the output of the four largest developing countries - Russia, India, Japan and China - was considerably lower than the deflation method yields. Clearly, the historical GDP reconstructions are not free of errors, either. Yet, if we decide to trust the accuracy of the work of economic historians, the market value of the output of low-income countries in 1914 must have been considerably lower. Adjusting developing countries’ GDP downwards, the ratio of foreign investment assets (or liabilities) to world GDP is likely to have been substantially higher than 20% - probably closer to 30%.

Schularick's implied $140 bn for current-price GWP in 1914 is the best published estimate I've seen, and offers a valuable warning of the shortcomings of projection from today's PPP-adjusted income levels. It's unfortunate that more historians don't adopt a similar approach of calculating current-price values from current-price data rather than recycling dubious estimates based on uncertain growth rates, questionable deflators and anachronistic aggregates.

Thursday 2 September 2010

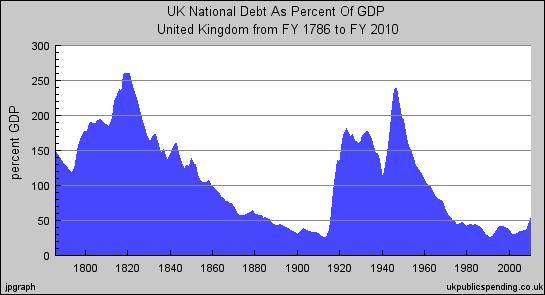

A debt disappointment

This handy chart of UK net public debt as a percentage of GDP is quite popular among those of us who like to point out that things have been far worse in the past:

Reassuringly in these days of government debt spiralling toward 70% of GDP, it shows that the UK debt-to-GDP ratio topped 250% in 1818-21, and we survived that.

But did it?

On closer examination of the data underlying the graph, the debt shown for the four peak years averages £841.5 million (from Mitchell), while GDP is estimated at £323.8m. But the latter figure seems substantially lower than other calculations based on contemporary estimates. Following Lowe, Deane & Cole reckon the GDP of Great Britain alone at £288m in 1821 - to which must be added Ireland's £70m or so - while Officer cites estimates in excess of £400m for the entire UK.

Consideration of the growth and price trends strongly supports the higher income figures. Deane & Cole certainly underestimated their 1865/85-price national product in 1801-21, and to a lesser extent to 1861. Prices in 1819-21 were falling rapidly from the high levels of 1800-18, but remained high in comparison with most of the ensuing century. Aggregate output c.1820 is in real terms unlikely to have been much under half of the £600m estimated for the UK in 1851, while prices were perhaps 30% higher.

So it seems that the post-Napoleonic War UK debt burden peaked at rather under than over two and a half times GDP - perhaps 235% on the basis of Deane's estimate and 210% or so according to some of the higher figures. It's still reassuringly higher than today's projected 70% - and we're unlikely to face 30 years of falling prices as we struggle to reduce the burden.

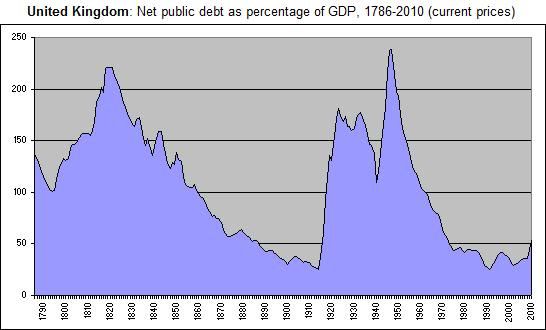

Later: Here’s my revised version of the chart, reducing the original’s annual current-price GDP rise by two-fifths in 1821-30 and by half in 1800-11, and assuming (fairly arbitrarily) growth of 4% in 1786-93 rising to 5% in 1793-1800 with the onset of wartime inflation. The absolute value of debt has been left unaltered throughout, as have the GDP estimates from 1830 to the present.

The peak ratio has now shifted from around 1820 to 1946-47 (237% and 238%). Price movements were certainly more helpful in bringing the burden down from the latter level: while it took until 1888 to get post-Napoleonic debt down to half of GDP, after World War II it took only until 1973.

Reassuringly in these days of government debt spiralling toward 70% of GDP, it shows that the UK debt-to-GDP ratio topped 250% in 1818-21, and we survived that.

But did it?

On closer examination of the data underlying the graph, the debt shown for the four peak years averages £841.5 million (from Mitchell), while GDP is estimated at £323.8m. But the latter figure seems substantially lower than other calculations based on contemporary estimates. Following Lowe, Deane & Cole reckon the GDP of Great Britain alone at £288m in 1821 - to which must be added Ireland's £70m or so - while Officer cites estimates in excess of £400m for the entire UK.

Consideration of the growth and price trends strongly supports the higher income figures. Deane & Cole certainly underestimated their 1865/85-price national product in 1801-21, and to a lesser extent to 1861. Prices in 1819-21 were falling rapidly from the high levels of 1800-18, but remained high in comparison with most of the ensuing century. Aggregate output c.1820 is in real terms unlikely to have been much under half of the £600m estimated for the UK in 1851, while prices were perhaps 30% higher.

So it seems that the post-Napoleonic War UK debt burden peaked at rather under than over two and a half times GDP - perhaps 235% on the basis of Deane's estimate and 210% or so according to some of the higher figures. It's still reassuringly higher than today's projected 70% - and we're unlikely to face 30 years of falling prices as we struggle to reduce the burden.

Later: Here’s my revised version of the chart, reducing the original’s annual current-price GDP rise by two-fifths in 1821-30 and by half in 1800-11, and assuming (fairly arbitrarily) growth of 4% in 1786-93 rising to 5% in 1793-1800 with the onset of wartime inflation. The absolute value of debt has been left unaltered throughout, as have the GDP estimates from 1830 to the present.

The peak ratio has now shifted from around 1820 to 1946-47 (237% and 238%). Price movements were certainly more helpful in bringing the burden down from the latter level: while it took until 1888 to get post-Napoleonic debt down to half of GDP, after World War II it took only until 1973.

Tuesday 31 August 2010

Pre-industrial England: The Uzbek connection

Gregory Clark has been at it again. In a recent paper with Joseph Cummins and Brock Smith, the neo-Malthusian enfant terrible of early modern English economic growth (or its absence) uses occupational evidence in wills to find a share of 60% of England's labour force in agriculture in both 1652-60 and 1560-79. This comes as no great surprise to those of us who've long held that the proportion was around half by 1700: in fact the new 17th-century estimate seems generous rather than shockingly low.

The paper gives some indication of the shares of some of the non-agricultural activities which by 1600 must have occupied something around half a million countryfolk, twice the urban labour force. But instead of pursuing this promising line of enquiry the authors go on to conjure up an estimate of per capita income based on agricultural employment shares and GDP in developing countries in 2007. England around 1600 had, we are told, a per capita income similar to Uzbekistan today, solely on the basis of a similar share occupied in agriculture - this from the scholar who (with considerable justification) condemned Angus Maddison's projections as "fictions... based not on empirical evidence, but on unsubstantiated and demonstrably implausible theories of the nature of life in pre-industrial societies". It's unclear quite what the Uzbekistan of 2007 is meant to tell us about pre-industrial England, except that most of its inhabitants by 1560 lived far above subsistence levels, which is hardly news. It's a promising paper, sadly derailed by its lead author's over-keenness to demonstrate the absence of significant per capita income growth before the Industrial Revolution.

Much the same goes for Clark's other new paper, on employment shares and income in the England of 1381. This time there's some of the occupational detail missing for the later period (like the author I was quite taken by the finding that 2.5% of those occupied in the sampled parishes were engaged in brewing) - and there's a real surprise, in the conclusion that only 55% of the labour force worked in agriculture (62% if all those returned as "labourers" and the like are assigned to farming), far lower than the 75% widely assumed to have been so occupied. The sample size is small - fewer than 3% of rural parishes and only two boroughs - and may over-represent smaller (non-borough) country towns at the expense of more strictly rural districts. But it's a thought-provoking illustration of the extent of late medieval rural crafts and commerce.

There's little evidence though for Clark's assertion on the basis of erratic wage and price data that English income per capita in 1381 averaged 94% of the 1817 level: again we're asked to put our faith in "modern data on income and farm shares across poorer countries" extrapolated according to a formula which yields an income elasticity of food demand "consistent with cross-sectional evidence for England in 1862" (at the end of what Greg and his then co-authors once aptly termed the "British food puzzle" of rising incomes and sluggish food demand in the Industrial Revolution period).

Taken together, these two papers offer a valuable insight into the English occupational history being researched elsewhere under Shaw-Taylor and Wrigley. It's frustrating that rather than use their occupational data to reconstruct the dimensions of real economic activity, the authors instead veer off into a mechanistic equation of occupational shares (and only one occupation at that) with GDP. Hopefully there'll be more detailed and nuanced investigation to follow.

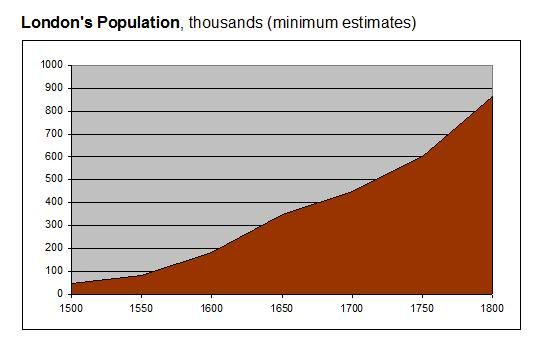

A dearth of Londoners

Just reading Mark Huberty on 17th-century London coal consumption, I was struck by the following:

Nevertheless, the data present an empirical puzzle. In 1600, London appears to have imported around 200,000 tons of of coal per annum for a population of approximately 100,000 people. In 1700, it imported around 500,000 tons for 500,000 people. In per capita terms, then, coal consumption appears to have fallen.

I think I can clear this up. I know of no estimate that puts London's population as low as 100,000 in 1600: the baptisms recorded in the Bills of Mortality indicate a minimum of 180,000 even before allowance for unrecorded births (my own preference is for something rather higher given rapid English population growth in 1500-1650 and near-stagnation in 1650-1730 coupled with a generally-accepted London population of 350,000 c.1650). To reach a population of 100,000 you probably have to go back at least to the 1550s. So it's likely that per capita consumption during the 17th century either remained stable or rose slightly (shipments in 1600 were probably rather under than over 200,000 tons and in 1700 conversely somewhat over 500,000 tons). So there's a definite slowing from the high per capita growth rates of the late 16th century - possibly related in part to movement of industry - but no significant drop in the absolute level of demand per head.

I think it's probably correct to say that the Fire of 1666 had little effect on London-wide take-up per capita: the coal data support the impression of slow growth in the late 17th-early 18th centuries, but beyond the exceptional impact of the 1665 Plague this is probably related to demographic developments not unique to London (as one would expect given the limited area affected by the conflagration). The already large volume of shipments does support the suggestion that coal use was the norm by the early 17th century, while the growth of shipments implies that this was a recent development (perhaps most marked in the quarter-century after 1580) associated with the metropolis's rapid expansion: indeed one might speculate whether that expansion would have been possible without the new wonder-fuel from the north given the prior claim of the south-east's million or so rural & small-town inhabitants to the region's stretched woodfuel resources.

What-o-philia??

Blame the late Angus Maddison who coined the term to denote his own fondness for historical number-crunching. Strictly it's "love of figures", though in reality it's curiosity about the dimensions of the past and present: How big? How many? How much bigger is it now than it was then? How quickly did it get there?

So what does a chiffrephile do? Well, they count and estimate, calculate and occasionally guess where there's nothing else to go on. They spend a lot of their time picking apart other people's numbers while hoping nobody notices the glaring holes in their own alternative method and results. And sometimes they'll try to make sense of what they've come up with, occasionally successfully.

This blog is in part a memorial to Maddison's own part in fuelling my own nascent chiffrephilia. It's also going to be a place for trying to come up with better data, as was Maddison's declared intention in publishing his own aggregates.

This then is a blog about quantity in history, from our earliest guesstimates up to the present. There'll be lot of picking apart others' findings, and hopefully I'll be able to offer better ones. And perhaps people with better numbers will come along and demolish mine. That's how we learn more.

Subscribe to:

Posts (Atom)