According to Kenwood & Lougheed (The growth of the international economy, 1971),

By 1913, the volume of foreign trade per capita had grown to over 25 times what it had been in 1800, whereas world output per head had grown only 2.2 times over the same period. This means that during the period 1800-1913 the foreign trade proportion, that is, the ration of world trade to world product, rose to over 11 times its initial level. Moreover, if, as seems likely, the world proportion of foreign trade to product was about 33 per cent in 1913, it must have been barely 3 per cent in 1800.

The authors were referring to total foreign trade, in other words the combined figure for exports plus imports. Since this totalled around $40bn in 1913, their implied world product works out at roughly $120bn. And as world population had nearly doubled in the meantime, their estimate implies for 1800 a world product approaching $28bn and trade totalling $0.8bn at 1913 prices.

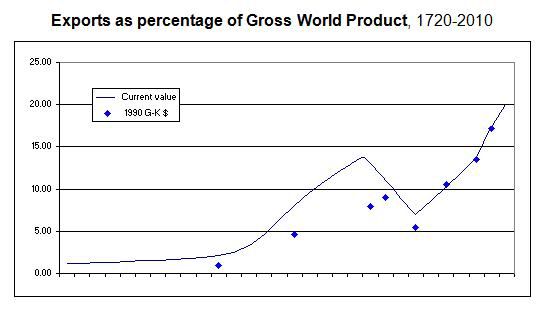

In 1995 Angus Maddison came up with a far lower ratio for 1913 of 8.7% of GWP for exports alone, which he lowered still further in 2001 to 7.9%, up from 1% in 1820 and 4.6% (originally 5%) in 1870. Since he also estimated current-price exports at $18.4bn in 1913 and $5.1bn in 1870, this implies a gross world product of $230bn in 1913 and $110bn in 1870, when prices were rather higher before the onset of the “great depression”. However, his ratios are computed at 1990 prices, which as we’ve seen aren’t necessarily the best guide even to the first half of the 20th century, let alone the 19th. Maddison offers no current-price figure for exports in 1820, but his volume estimate broadly agrees with Mulhall’s sterling value for total world trade in suggesting around $0.8bn - a value that is difficult to reconcile with Maddison’s 1% share of GDP, even given the eccentricities of 1990 Geary-Khamis dollar projections and the high prices of the 19th century’s opening decades.

Maddison’s estimates have become the standard in much of the literature, notably in recent work by Kevin O’Rourke, Jeffrey Williamson and Alan Taylor, who use them to show that exports grew more rapidly relative to GWP before 1913 than since. But are they reliable? The answer depends on what we’re measuring. As independent projections of two distinct variables from a 1990 base they may each possess some validity. But whether the resulting ratio corresponds to reality is another matter.

Fortunately a check is available, in the form of current-price data for leading countries and estimates of world trade at both current and constant prices from the 1870s. To take the most obvious case, the exports of Britain - the leading trading nation of the 19th century - are put by Maddison at 3.1% of GDP in 1820 and 12.2% in 1870. But at the prices of the time, the proportion (excluding re-exports of £10m and £45m) rose from around 9% to a fifth. For the US, exports reached 3.7% of GDP in 1913 according to Maddison’s series, but at that year’s prices were around 6½%: the corresponding ratio for Germany is likewise understated by upwards of a fifth, for France by half; China fares still worse, even reckoning GDP at the most generous level compatible with likely output.

Mulhall’s trade data on the other hand appear consistent both with Maddison’s current-price data and with the British returns extending back through the 18th century. His figures include Britain’s large re-export trade and presumably the transit trade of the Netherlands whose inclusion as undifferentiated exports irked 20th-century international statisticians, but they can be adjusted for both. He also combines imports and exports, so his totals need reducing by more than half to omit not only the double-counted merchandise but also freight & insurance costs. Expressed as a percentage of current-price world product, the results were combined with post-1870 data to yield the following decennial series (except 1913, 1929 and 1937):

The current-price estimates indicate that the 1990 G-K dollar data grossly understate exports relative to GDP in 1820, 1870 and 1913. The 1% level was probably reached around 1700 rather than 1820, when the real ratio was about 2%. The 1870 ratio similarly already exceeds Maddison’s 7.9% for 1913, when the true figure reached 13%. The discrepancy extends to 1950, for which Maddison inexplicably reduced his already somewhat low 7% to a calamitous 5½%.

Kenwood & Lougheed on the other hand seem to have been remarkably accurate all those years ago with their estimate of world output in 1800 (assuming that they started from accurate trade & population figures for 1913), though they underestimated both trade in the earlier year and GWP in the second. The intervening rise in the export ratio was not elevenfold but probably slightly less than eightfold.

While Mulhall's early estimates doubtless contain an element of approximation, this is not sufficient to greatly alter the conclusion, and there is no indication that he overstated "unknowns": if anything, non-western countries' share looks likely to be understated. Furthermore, the finding of far larger early-modern trade is supported by still earlier estimates such as Braudel's astonishing tenth of national income (upwards of 0.4% of world product) for 16th-century French imports (a good part doubtless for re-export).

One peculiarity of the Maddison series is its suggestion that exports outstripped world output in 1913-29, a notion which would have surprised contemporary experts: in fact at current prices the 1913 percentage was not surpassed until the 1973 oil price rise raised the total to $850bn - a still more shocking finding that calls for future investigation but which in view of postwar western liberalisation would seem to reflect faster intervening growth in services and in output of less trade-dependent regions more than policy or failure of the trading system.

In terms of volume, the data illustrate four familiar stages of export growth over the past 300 years: an annual increase of about 1% to c.1815, an acceleration to 3½% in the following century and then a period of near-stagnation from 1914 until the resumption of rapid growth from the mere $37bn of 1946, leading to the 5-6% annual increases of recent decades. Comparison of the century to 1913 with the one after is uninstructive as the second comprises three decades which form part of neither suggested period of globalisation: of these, the last showed faster growth, but the earlier trade surge produced a sevenfold rise in exports’ share of gross product.

On a speculative note, compared to Maddison's more linear 1820-1929 trend, the slowing of export growth from the high rates of 1830-60 lends the current-price estimates the appearance of a flattened S-curve interrupted in 1914 and with which the subsequently disrupted export/GDP ratio is only now once again intersecting as it approaches the former's implied upper bound of perhaps 30%. The slowdown of 1861-1913 of course owes much to the successive impacts of the US Civil War, the 1873-96 price depression and the rise of protection, but each of these in its own way reflects trade-related stresses suggestive of a finite tolerance for commercial openness at the aggregate global level. Much has of course changed in the intervening century, but it remains to be seen whether the 21st century resumes the trend of the 19th or continues that of the late 20th.

It seems clear that in real terms international merchandise trade was more significant in the early 19th century than the currently-accepted estimates allow for. That still means that nearly 98% of output supplied domestic demand in 1820, 99% in 1700. But the world was already a little more “global” than we’ve been led to believe, and was to remain so into the comparatively recent past. The resulting flattened growth trend may be indicative of future limits to trade globalisation, or of an ongoing structural break with past centuries.

No comments:

Post a Comment