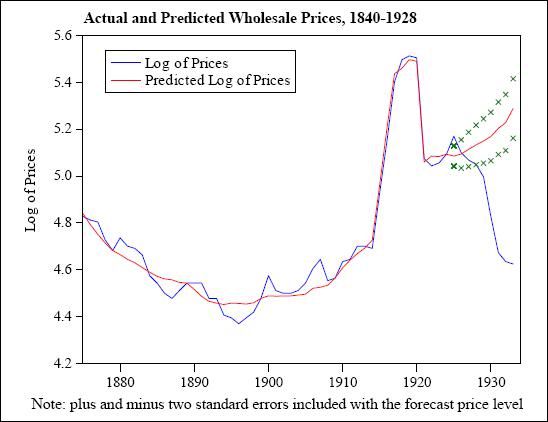

Irwin doesn’t at all exonerate US monetary authorities of their share of responsibility for the slump: rather he finds that while the two countries were equally to blame in the first half of the period, France was the culprit after the US reversed its own gold hoarding in 1931. It’s not an entirely novel perspective: Irwin cites contemporary expert warnings of the dangers of French & US conduct even as prices seemed to be stabilising in 1928 and the first half of 1929. What’s new is his finding that world prices would have risen in 1929-33 rather than plunging, had France and the US merely maintained their 1928 ratio of reserve gold to money supply. The associated graph is striking, but not entirely convincing: for one thing, it doesn’t explain falling prices in 1925-28, when French and US gold holdings were reasonably well-behaved and world gold reserves rising broadly in line with economic output; it also doesn’t show what the projected price trend would have been under the same assumptions but with no additional monetary gold from 1928, as was effectively the case. Even with the average world economic growth rate of around 3¾% annually over 1922-29, an absence of extra “active” gold would seem insufficient to account for the scale of the subsequent collapse of prices – and that’s before taking into account the reversal of real output growth in the early 1930s. But it certainly didn’t help.

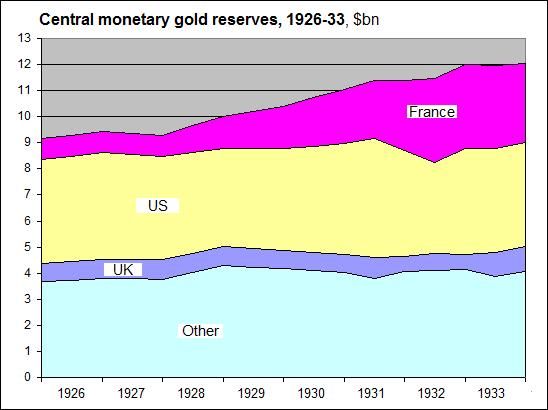

In fairness to the French, it should be remembered that despite converting a large part of its sterling holdings into gold from 1927, the Banque’s reserves still suffered through Britain’s effective 30% devaluation in 1931. If – as most commentators seem to agree – sterling was indeed overvalued by something like a tenth in 1925, then gold indeed made more sense than at least one of the world’s notional reserve currencies. French gold hoarding of course contributed to sterling’s difficulties, so it’s not much of an excuse. And the franc was itself widely regarded as undervalued from 1928, making the country already a gold sink. Though cushioned to some extent against the first impact of the 1929 global economic downturn, France was to pay dearly for its attachment to gold as she entered the worst phase of the depression just as many countries were starting to climb out of it in 1933: not until 1936 did the country finally free itself of what Keynes had dubbed the gold “fetish”, the last power to do so. By 1938 France’s share of world gold reserves was down from its 1932 peak of 28% to just a tenth.

What are we to make of it all? Well, for one thing proclaiming a new international regime doesn’t make it so without the mechanisms to implement it. Could the gold exchange standard have worked as envisaged at Genoa in 1922? For a time, no doubt, with better alignment of the key currencies and binding undertakings to play the game: supply of the required metal was to prove adequate in the 1930s, as it could have been in the 1920s. But by then it was too late: the inflexibility implicit in the attempt to return to gold and the impossibility of ensuring its optimal distribution had crippled not just the monetary system but the wider economy. Would a more internationally-minded Banque de France have spared the world the nightmare of Depression and war? Possibly not: there was far more amiss in the interwar economy than just monetary policy and gold stocks. France may not have caused the Depression, but it made things a lot worse.

No comments:

Post a Comment